US tariffs on the least developed countries amount to an assault on already marginalized populations.

Daniel Gay

Publication Date

08 April 2025

The US tariffs unveiled on Wednesday will hit all 44 of the world’s least developed countries (LDCs), in some cases slashing economic growth and lowering employment—with a potentially serious impact on livelihoods.

From 9 April, 31 of these countries will face a tariff rate of 10%, while in the remaining 13 rates range from 11% in Democratic Republic of the Congo, to 50% in Lesotho.

For some countries, the shock will be severe. The affected African exporters will move from zero duties under the African Growth and Opportunity Act (AGOA), to high rates. Several of these countries depend heavily on access to the US market.

Other LDCs, like Bangladesh and Cambodia, will shift from special LDC concessionary levies at or near zero, to much higher rates—37% in Bangladesh and 49% for Cambodia.

This big new tax on every Cambodian or Bangladeshi T-shirt crossing the US border will dramatically increase costs and put those industries under strain.

The move represents a major break from the last two decades, when LDCs were given duty-free, quota-free access to many major markets, including the US, as part of a concerted international push to integrate the world’s least advantaged nations into the global economy.

The move represents a major break from the last two decades, when LDCs were given duty-free, quota-free access to many major markets, including the US, as part of a concerted international push to integrate the world’s least advantaged nations into the global economy.

These efforts met with mixed success, but now, just as these mostly small, poor countries are struggling to recover from the catastrophe of Covid-19 and the supply chain and inflation crisis, they’re being pushed down even further. Never mind kicking away the ladder; it’s a case of holding their heads under water.

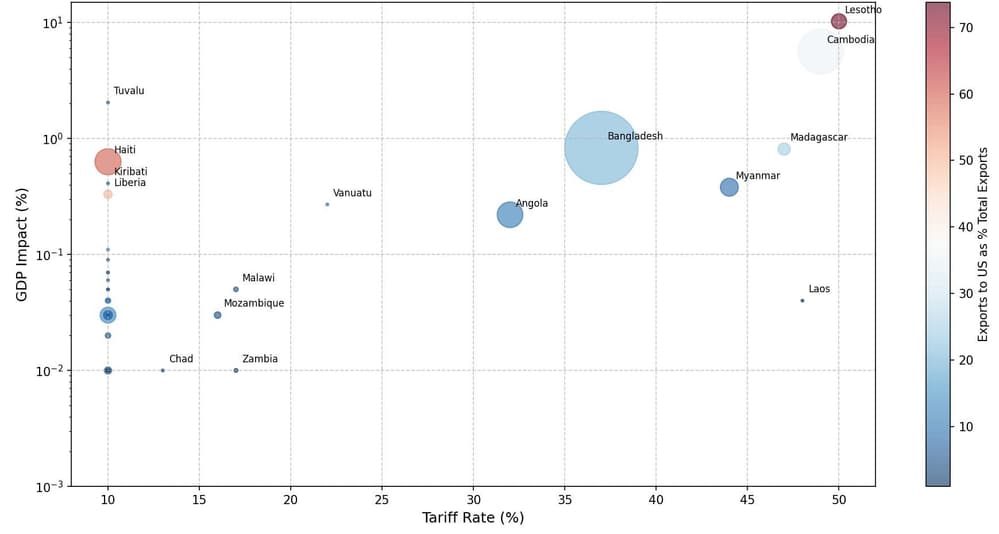

My initial calculations on the possible impacts are shown in the following figure.

Impact of US Tariffs on Least Developed Countries

Data source: OEC

Note: The y-axis is the log of the estimated impact on GDP, in percentage terms. The x-axis is the % tariff rate faced by each LDC. The size of each bubble represents the log of total exports to the US, while the colour, from blue to red, signifies the proportion of the country’s exports going to the US.

In the basic model used to make the calculations, I assume an elasticity of -0.75 for garments. Studies suggest that a 1% price increase reduces apparel demand by 0.5% to 1% (an elasticity of -0.5 to -1). So assuming na elasticity of -0.75, half way between these levels, a 50% price increase could reduce demand in Lesotho by 37.5% (0.75 × 50%), a loss of $120 million. Garments are easily substitutable, so this seems plausible. For commodity exporters like Angola and DR Congo I assume a lower elasticity of -0.4. I also assume that the impact of reduced spending on each economy multiplies the impact by 1.5 to 2.

Clearly this is a very basic model put together quickly that hasn’t been academically reviewed, and doubtless has shortcomings. But it serves as a rough guide as to which countries will be affected worst, together with the magnitudes.

Lesotho will suffer worst, given the dependence of the economy on exports to the US, mostly garments. Lesotho’s $2.05 billion economy sends approximately $320 million in garments to the US, or three quarters of all exports, manufactured in zones near the capital Maseru, which are run by Chinese and Taiwanese investors.

About 36,000 people work in these factories, which provide much-needed employment in a country where the poverty rate tops half of all people. This is a poor and vulnerable country which desperately needs all the help it can get. For example, when I last visited about a dozen years ago, average life expectancy was only 47. Now, it has risen, but to only 53, one of the lowest levels in the world.

The overall impact on Lesotho’s GDP could be as high as 10%. Of course manufacturers might switch some production elsewhere, but supply chains are most likely carefully designed to meet the exact demand of US consumers, and new markets won’t easily be found, especially when other garment exporters are facing the same situation.

Instead of cutting jobs, employers might try to furlough workers or pay them less—although neither of these options would be good. It is quite possible that investors will simply shut up shop and move elsewhere. The industry is surprisingly footloose, with relatively low capital outlays and basic skill levels.

Because of the poor design of the tariffs and the fact that they are somewhat arbitrary, some countries may just shift production to a low tariff neighbour and carry on as usual. Might an African neighbour benefit? Trump doesn’t seem to know about rules of origin. Either way, the impact could be disastrous.

Cambodia is also going to get hammered unless something changes. About 35% of its exports, also mostly garments, go to the US. That’s about 8.7% of GDP. My basic calculations suggest that the impact on GDP could be as much as 5%—not as bad as Lesotho but still highly destabilizing in a poor country with limited opportunity for diversification and facing fierce competition.

Madagascar’s vanilla exporters are also likely to suffer. About a quarter of the country’s exports go to the US and it faces a 47% tariff.

Laos, Bangladesh, Myanmar, and Angola equally face a potentially severe impact. All either meet the criteria to graduate from the LDC category or are imminently scheduled to do so. The US tariffs will set back their cause.

Bangladesh is the world’s second-largest garment exporter and the industry has propelled the country to high rates of economic growth in recent years, leading to poverty reduction of as much as 50 million.

Against the backdrop of the country’s recent regime change, the huge garment industry needs to be supported, not undermined. Although Bangladesh did not benefit significantly from the US duty-free, quota-free scheme, the 20% of exports that go to the US cannot quickly switch to Europe.

During my visits to Dhaka, business leaders told me they could cope with the few percentage points tariff increase that may come through LDC graduation, but presumably not 37%. It will be workers who pay, not factory owners.

Over 3000 people have died in Myanmar following the recent earthquake. However poisonous the regime, slapping the country with a 44% tariff at this time seems positively cruel. European investors told me when I went to Naypyidaw and Yangon before the 2021 coup that the country was already barely competitive in garments, and risked losing business to more stable and cheaper Asian neighbours.

The same goes for Haiti. 60% of its exports—again garments—go to the US. The country is reported as being essentially ungovernable, with gangs controlling large parts of the capital, Port-au-Prince and the economy in freefall.

Although the US tariff is “only” 10%, it will still have an impact on an already desperate situation, given the volumes involved, the dire need for jobs, and the undiversified nature of the economy.

I worked in Haiti during Hurricane Sandy in 2012, and only on a few occasions have I been amidst such destruction, and seen such hopelessness. Things have got worse since then. Inflicting more pain on a country where nearly 60% live below the poverty line seems simply abusive.

A Devastating Failure

Most LDCs will escape any major impact because they do not export much to the US, total exports were minimal, or the proposed tariff is low—or some combination of the three. Several did not benefit much from the US duty-free scheme anyway.

Some LDCs might be able to switch exports to other markets. Doubtless, China will swoop in to buy more from the commodity producers. The EU is already preparing to receive a flood of goods previously destined for the US market but which will now be diverted.

But overall, in the eight or more counties where the tariffs will have a major impact, jobs at risk could total as many as 380,000—mostly in Bangladesh and Cambodia, but also elsewhere. Any job in an LDC is a hard-won prize, and replacing lost employment is often much harder than in richer, more diversified countries.

Any job in an LDC is a hard-won prize, and replacing lost employment is often much harder than in richer, more diversified countries.

The loss of export revenues could reach as much as a quarter of the total from LDCs unless something changes.

For Lesotho and Myanmar the potential economic impact will be severe and possibly even unmanageable. LDCs do not have unemployment benefits and most people have no or minimal savings. And this is on top of US aid cuts, which are already biting hard.

What is horribly ironic is that the tariffs on these countries will not even benefit the US, which is not quickly going to bring back garment production—nor should it want to. US workers will not graft for six days a week making T-shirts for $100 a month, as Bangladeshis do.

The US cannot even produce some of the things it is supposedly “protecting.” Good luck growing bananas or coffee. The tariffs will mean higher costs for US businesses and consumers.

And the collective trade surplus of the LDCs with the US amounts to only 0.001% of the US trade deficit, so will make absolutely no difference to Trump’s stated aim of “balanced” trade—not that tariffs will do so anyway.

In sum, these half-baked and poorly-thought-out tariffs, which will raise rates to the highest in over a century, will not only fail, but will needlessly inflict yet more pain on populations that were already suffering from severe poverty and deprivation.

The latest moves amount to nothing other than an attack on the world’s poor.

* This piece was originally published on dangay.substack.com and has been edited for Synergies.

----------

Daniel Gay is an advisor on trade and development. He has previously worked at the UN Committee for Development and the Organisation for Economic Co-operation and Development. His books and articles are on economic methodology, trade, and sustainable development and can be accessed here.

-----

Synergies by TESS is a blog dedicated to promoting inclusive policy dialogue at the intersection of trade, environment, and sustainable development, drawing on perspectives from a range of experts from around the globe.

Disclaimer

Any views and opinions expressed on Synergies are those of the author(s) and do not necessarily reflect those of TESS or any of its partner organizations or funders.

License

All of the content on Synergies is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0)

license. This means you are welcome to adapt, copy, and share it on your

platforms with attribution to the source and author(s), but not for

commercial purposes. You must also share it under the same CC BY-NC-SA

4.0 license.